What if the biggest hurdle between you and your first set of keys isn't actually your savings account, but simply knowing how to claim the first home owners grant qld? It's completely normal to feel a bit frazzled by the mountain of paperwork and "government-speak" that usually comes with buying property. You're likely staring at your bank balance and wondering if you'll ever have enough for a deposit, or if you should give up on that dream build and just buy something established instead. I hear you, and you're definitely not alone in feeling that way.

The good news is that the grant is still sitting at a life-changing $30,000 for 2026, and it's designed to get you through your new front door much faster. I've put this guide together to show you exactly how to secure that cash without the usual headache. We'll walk through the latest eligibility rules, explain how you can skip stamp duty entirely, and give you a clear, step-by-step plan to get your application sorted. It's time to stop worrying about the jargon and start planning your housewarming party.

Key Takeaways

- Discover how the $30,000 first home owners grant qld works as a direct government gift to help you build or buy your brand-new home sooner.

- Check the simple "First Timer" checklist to ensure you and your partner qualify for the full amount based on your residency and property history.

- Learn how to combine the grant with stamp duty concessions to potentially pay zero tax on your new purchase.

- Find out how to pair state support with federal schemes to get into your home with as little as a 5% deposit and no LMI.

- Get a clear, step-by-step plan for the application process so you know exactly which documents to grab before you sign any contracts.

Queensland First Home Owners Grant: What is it in 2026?

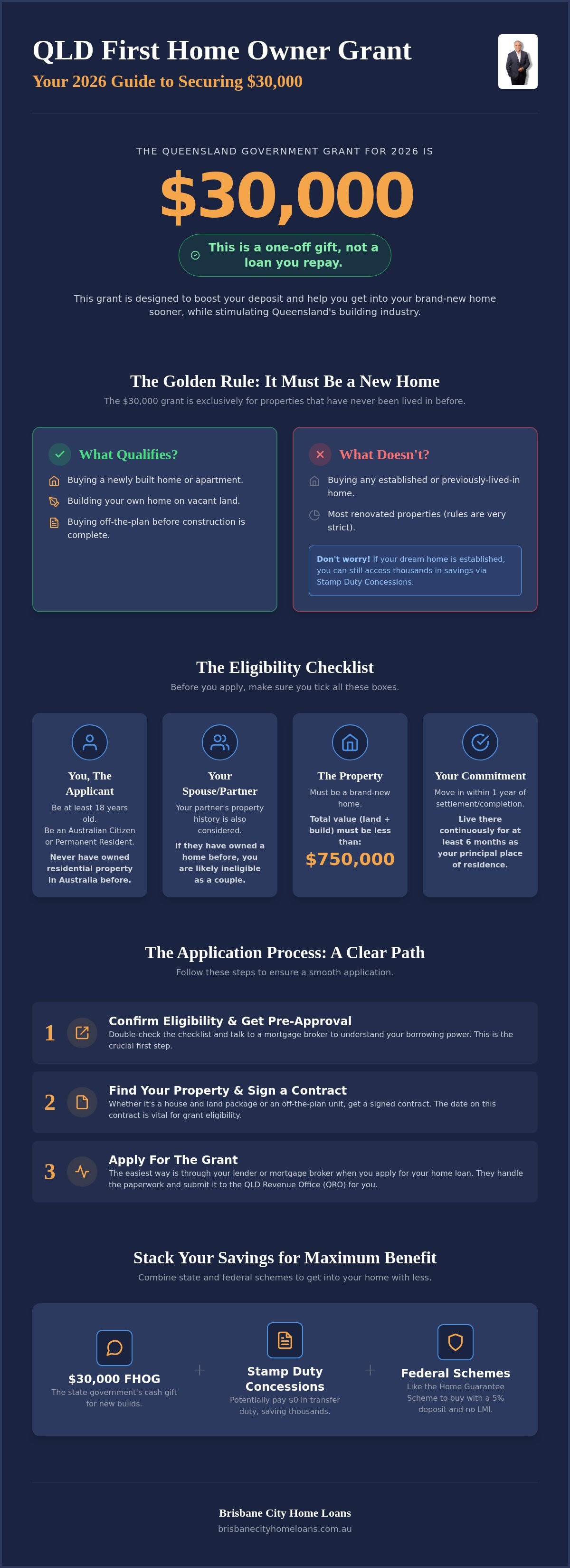

Think of the First Home Owners Grant (FHOG) as a massive leg-up from the Queensland Government. It isn't a loan that you have to pay back with interest over the next thirty years. It's a one-off gift of cold, hard cash designed to help you cross the finish line of your savings goal. Whether you're dreaming of a sleek apartment in South Brisbane or a family home in Townsville, this grant is there to make that first step onto the property ladder feel a lot less like a giant leap.

The headline figure for 2026 is $30,000. That is a significant chunk of change that can go directly toward your deposit or the costs of finishing your home. Why is the government being so generous? It's pretty simple. Queensland is growing fast, and we need more rooftops. By offering the first home owners grant qld, the state encourages builders to keep hammering away at new projects, which helps increase the overall housing supply for everyone. It's a win-win that puts you in a brand-new home while keeping the local building industry humming.

The 2026 Update: Is the $30,000 Grant Still Available?

You might have heard rumours about the grant "expiring" or changing. Here is the deal: the grant was originally doubled from $15,000 to $30,000 back in November 2023. While it was initially a temporary boost, the Queensland Government confirmed in the 2026-27 State Budget that the $30,000 amount is here to stay for the current financial year. As long as your contract is signed on or after 20 November 2023, you can still access the full amount. It's a great relief for anyone who felt they might have missed the boat.

New Home vs. Established: The Great Divide

There is one very important rule you need to know: this grant is strictly for brand-new homes. If you've been eyeing off a beautiful 1970s Queenslander with heaps of character, the $30,000 first home owners grant qld won't apply there. To qualify, the property must be one that has never been lived in before. This includes:

- Buying a home that has just been built.

- Buying "off the plan" before the building even exists.

- Building your own home on a vacant block of land.

- Purchasing a home that has undergone "substantial renovations" (this is rare and has very strict rules).

If your heart is set on an older home, don't feel discouraged. While you won't get the $30,000 cash injection, you can still save thousands through stamp duty concessions, which we'll break down for you later in this guide.

Are You Eligible? The QLD FHOG Checklist

So, do you actually qualify for the $30,000? It is the question everyone asks first. The first home owners grant qld isn't just handed out to anyone. There are a few boxes you need to tick to make sure you're eligible. It is best to check these before you get your heart set on a specific floor plan or start picking out kitchen tiles.

Individual Eligibility: The Basics

You need to be at least 18 years old and a real person. In the eyes of the law, that means you're a "natural person" rather than a company or a trust. At least one person on the application must be an Australian citizen or a permanent resident. But what about your partner? This is where it gets a bit sticky. If you're buying with a spouse or de facto partner, and they have owned a home in Australia before, you usually won't be able to claim the grant. Even if you've never owned a single brick, their history counts toward the eligibility criteria. It is a "one strike and you're out" rule for the whole household.

Property Eligibility: The $750k Limit

The total value of your new home must be less than $750,000. This includes the land and the cost of the build combined. If you're buying a house and land package in a growing suburb like Pallara or Ripley, you'll need to keep a close eye on the final price. Every extra upgrade or variation can push you closer to that limit. In Brisbane, this cap can feel a bit tight compared to a few years ago. You might find your dollar goes much further in regional areas like Toowoomba or the Fraser Coast. If you're buying off-the-plan, the valuation is based on the contract price. Make sure you've got a clear figure before signing anything. If you're feeling unsure about how your budget fits these limits, chatting with the experts at Brisbane City Home Loans can help you stay on track.

The Residency Requirement

Once the build is finished or you've settled on the home, you can't just rent it out immediately. You must move in within 12 months of the completed transaction. Once you're in, you need to live there as your main home for at least six months straight. The QRO is quite strict about this. They want to see that you're actually living there. They might check where your mail is delivered or where you're registered to vote. If you move out too early or never move in at all, you'll likely have to pay the full $30,000 back. It is about making sure the first home owners grant qld helps people find a place to call home, not just an entry into the rental market.

Grant vs. Concession: Understanding Your Savings

It is very common to get these two mixed up. They both sound like "free money" from the government, right? While they both help your bank balance, they work in different ways. The first home owners grant qld is a cash payment that lands in your account (or goes to your builder) to help with the costs of a new home. A concession, however, is a discount on the tax you would usually pay when buying property. In Queensland, this tax is officially called "transfer duty," but most of us still just call it stamp duty.

The best part is that you can often "double dip." If you are building or buying a brand-new home, you can grab the $30,000 cash grant and pay zero stamp duty at the same time. Even if you decide to buy an established home and miss out on the cash grant, you might still be eligible for the tax discount. It is the government's way of making sure first-time buyers have a fighting chance, regardless of whether they want a shiny new build or a cottage with some history. You can see the full breakdown of these rules on the official page for the Queensland First Home Owner Grant.

The First Home Concession Explained

Since May 2025, the rules have become much friendlier for your wallet. If you are buying a new home or building on vacant land, you are now fully exempt from stamp duty. There is no property value cap for this exemption on new builds, which is a huge win. For those buying an established home, you won't pay a cent in stamp duty if the property is under $700,000. If the price is between $700,001 and $799,999, you still get a partial discount. For a deeper look at all the different types of help available, check out our guide on the First Time Buyer Grant QLD: Your 2026 Guide to Government Support.

How Much Could You Save Total?

Let's look at a quick example to see how the numbers stack up. Imagine you're buying a new house and land package for $650,000. Because it's a new build, you'd get the $30,000 first home owners grant qld. On top of that, you would normally pay around $22,000 in stamp duty, but as a first home buyer, that is now zero. That is a total benefit of $52,000! While banks still want to see that you've saved some of your own money (what they call "genuine savings"), having this extra $52,000 in your corner makes the whole process much easier.

Andrew’s tip: While these savings are amazing, don't forget to keep a bit of cash aside for the "boring" stuff. You will still need to budget for things like building and pest inspections, legal fees for your solicitor, and the cost of the moving truck on the big day. It is always better to have a small buffer so you aren't stressed during your first week in the new place.

The Step-by-Step Application Process

Applying for the first home owners grant qld shouldn't feel like you're sitting a university exam. Most people think they have to wait until they've already bought the house to start the paperwork, but that's a bit like trying to put on your seatbelt after you've already started driving. You want everything ready to go well before you find "the one." Starting the conversation early means you won't be scrambling for documents while you're trying to negotiate a price with a builder.

To get the ball rolling, you'll need to gather a few essentials. The Queensland Revenue Office (QRO) is big on proof, so make sure you have your ID (like a passport or driver's licence), your signed contract, and proof of your citizenship or residency status. You'll also need to sign a statutory declaration. This is just a formal way of saying you've never owned a home before and that you're telling the truth about your application. It sounds serious, but it's a standard part of the journey.

Applying Through Your Mortgage Broker

This is where Andrew makes your life much easier. Instead of you wrestling with government portals and confusing forms, he handles the heavy lifting as your "Approved Agent." He makes sure your grant application is perfectly synced with your first home buyers qld loan approval. This avoids those heart-stopping moments where the bank says "yes" but the grant office asks for more info. Andrew checks every signature and date to ensure your application sails through without the usual delays that trip up solo buyers.

Payment Timing: When Do You Get the Cash?

Wait, when does the money actually land in your account? This is the part most websites gloss over. If you're buying a brand-new "spec" build or an off-the-plan apartment, the $30,000 first home owners grant qld usually arrives at settlement. This means the cash is there on the day you get the keys. However, if you're building your own home on a block of land, the timing is a bit different. The funds are typically released when the foundations (the slab) are poured. This is usually the first "draw-down" payment your bank makes to the builder.

One quick warning: don't rely on the grant for your initial 5% or 10% deposit. You usually need that cash upfront to sign the contract, but the grant money isn't released until much later in the process. It's a fantastic boost for your overall equity, but it won't replace the savings you need to get the ball rolling. If you want to make sure your finances are ready for the big move, you can chat with Andrew today to get a clear plan in place.

Maximising Your Support: Beyond the FHOG

While the $30,000 first home owners grant qld is a massive help, it is often just one piece of the puzzle. If you are trying to buy in a competitive market like Brisbane or the Gold Coast, you might still be worried about the size of your deposit or the extra costs of borrowing. The good news is that there are other programs out there designed to sit right on top of your state grant. When you stack these different types of support together, that dream of home ownership starts to look a lot more like a reality.

The trick is knowing how to make these different schemes play nicely together. You don't have to choose just one. In many cases, you can claim your state cash, skip the stamp duty, and use a federal guarantee to lower your deposit requirements all at the same time. It is about layering your options to create the best possible outcome for your specific budget.

Federal Government Schemes

The big one to watch for is the First Home Guarantee. Usually, if you have less than a 20% deposit, banks will charge you a hefty fee called Lenders Mortgage Insurance (LMI). This can cost you tens of thousands of dollars. However, under this federal scheme, the government acts as your guarantor. This allows you to buy a home with as little as a 5% deposit without paying a cent in LMI.

These national programs work perfectly alongside the first home owners grant qld. While the state grant gives you the cash, the federal guarantee makes it easier to get your loan approved with a smaller nest egg. Just keep in mind that federal schemes often have their own income caps and property price limits that might differ slightly from the state rules. It is important to check both sets of fine print before you get too far down the road.

Why Use a Local Brisbane Broker?

You could walk into your local big bank branch, but they can only tell you about their own products. They won't tell you if the bank across the street has a better deal for first-time buyers. As a broker, Andrew has access to over 60 different lenders. He can compare hundreds of loan products to find the "sweet spot" where the grant, the federal schemes, and your personal budget all meet.

Buying your first home should be an exciting milestone, not a source of constant stress. Andrew's approach is all about taking the weight off your shoulders. He handles the lender negotiations, organises the paperwork, and makes sure you're getting every bit of support you're entitled to. We are here to guide you through the whole maze from start to finish, ensuring you feel confident and comfortable every step of the way.

Ready to see if you qualify? Book a free chat with Andrew today.

Your Path to a New Front Door Starts Here

Securing your first home doesn't have to be a high-stress mission. By now, you've seen how the first home owners grant qld can bridge that deposit gap and how combining it with stamp duty concessions can save you a small fortune. Whether you're building in the suburbs or buying a new apartment in the city, the support is there to help you stop renting and start owning. It is all about having a clear plan and knowing which buttons to press.

You don't have to figure out the fine print on your own. Andrew brings years of local Brisbane expertise to the table and can compare over 60 lenders to find the perfect fit for your budget. The best part? His service comes at zero cost to you as the borrower. If you're ready to clear the confusion and get moving, book a free, no-obligation consultation with Andrew today. You're closer to those new house keys than you think, and we can't wait to help you get there.

Common Questions About the Grant

Can I use the QLD First Home Owners Grant as my deposit?

You generally can't use the grant as your initial deposit because of the timing. Most builders and sellers want their 5% or 10% deposit when you sign the contract, but the grant money isn't paid out until settlement or when the slab is poured. It is a great help for your total equity and reduces your overall loan amount, but you will still need some of your own savings to get the ball rolling.

What happens if I move out of the house within the first year?

You will likely have to pay the full $30,000 back if you move out before you have lived there for six months straight. The residency rules are quite clear: you must move in within 12 months of settlement or completion and stay put for at least half a year. If your life circumstances change suddenly, it is vital to contact the Queensland Revenue Office to discuss your options before you pack your bags.

Can I get the grant if I am buying an established house that has been renovated?

Standard renovations on an older home won't qualify you for this grant. To get the cash, the property must be officially classed as "substantially renovated," which means the home was almost entirely rebuilt and has not been lived in by anyone since the work was finished. A typical "flip" where someone has just updated the kitchen and bathroom of a 1980s house won't tick the boxes for this specific support.

Does the grant apply to house and land packages in Brisbane?

Yes, house and land packages are one of the most common ways to claim the first home owners grant qld. As long as the combined cost of your block of land and your building contract stays under the $750,000 limit, you are eligible to apply. This is a fantastic option for buyers looking at new estates across Brisbane where you can pick your own floor plan and finishes from scratch.

How long does it take for the QLD First Home Owners Grant to be approved?

Approval usually takes about one to two weeks once your broker or lender has lodged all the correct paperwork. If you apply through an approved agent, they do a lot of the pre-checks for you, which helps avoid the back-and-forth that can slow things down. While the approval happens fairly quickly, remember that the actual funds aren't released until your home reaches the required milestone, like settlement or the slab pour.

Can I get the grant if I have owned an investment property before?

No, you cannot claim the grant if you have owned any residential property in Australia before. The government's "first timer" rule is very strict and includes investment properties, even if you never spent a single night living in them. If you have previously owned commercial property, like a warehouse or an office space, you might still be eligible, but any previous home ownership will unfortunately count you out.

What is the maximum property value for the FHOG in QLD for 2026?

The maximum property value for the first home owners grant qld is $750,000. This total must include the price of the land plus the cost of the build and any variations you've added during the process. If your final contract price goes over this cap, you won't be able to claim the $30,000, so it is really important to keep a close eye on your budget during the design phase.