Does your heart sink a bit when you see a news alert about the RBA pop up on your phone? You aren't the only one. It feels like every month there is a fresh headline about the rba cash rate and another reason to worry about your household budget. With the official rate held at 4.35% as of July 2026, many Brisbane families are wondering when they will finally get a breather.

It is exhausting trying to translate banking jargon while your mortgage repayments keep creeping up. You deserve to feel like your bank is giving you a fair go, rather than just sending you another bill you can't control. This guide is here to clear the air and put you back in the driver's seat. I will explain exactly how these national decisions impact your specific home loan and, more importantly, what you can do to protect your wallet. We will look at the real difference between the official rate and what your bank actually charges you. I will also share the practical steps you can take right now to lower your own interest rate and keep more of your hard-earned money.

Key Takeaways

- Understand why the 4.35% rba cash rate is just the starting point and what the 2026 "levelling out" phase means for your family budget.

- Learn why your bank doesn't always follow the RBA's lead and how to spot the "loyalty tax" hidden in your current home loan.

- Find out where your real interest rate is hiding on your bank statement and why that number is the one that actually matters.

- Get a simple plan to use an offset account so you can pay less interest to the bank every single day.

- Discover how having a local expert compare over 60 lenders can help you find a better deal without it costing you a cent.

What is the RBA Cash Rate and Why Should You Care?

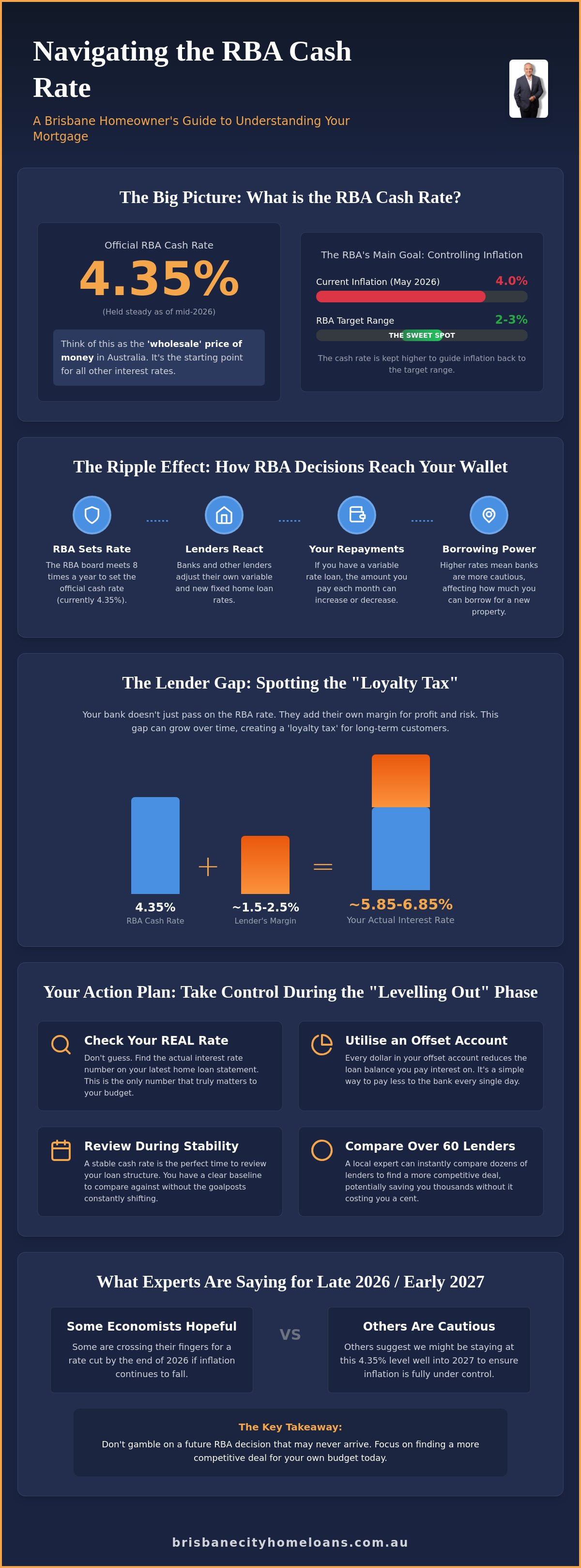

Think of the cash rate as the "wholesale" price of money in Australia. Just like a local grocer buys fruit at a wholesale market before selling it to you, your bank "buys" money at a price influenced by the Reserve Bank. If the wholesale price goes up, the price you pay for your mortgage usually follows. The Reserve Bank of Australia (RBA) uses this rate as a steering wheel to keep our economy on the right track. Their main goal is to control inflation and keep things stable so we don't end up in a boom-and-bust cycle that hurts everyone.

When the RBA changes this rate, it isn't just a number on a spreadsheet. It creates a massive ripple effect that eventually hits your bank account and changes how much you have left for the school run or the weekend barbie. For Andrew, the rba cash rate is the primary tool he uses to gauge which lenders are currently being fair and which ones are being a bit cheeky with their margins. It helps him see through the marketing fluff and find the real value for Brisbane families.

How the RBA Makes Decisions

The Monetary Policy Board doesn't just make these calls on a whim. They meet eight times a year according to the 2026 schedule to look at how we are all doing. They check if we are still spending at the shops, if people are finding jobs, and how fast the cost of living is rising. If you want to look at the global context, you can read more about What is the Official Cash Rate? to see how it works. Every meeting day, the decision is announced at exactly 2:30 pm. It's the moment when every homeowner in Queensland stops what they're doing to check the news.

The Ripple Effect on Your Mortgage

Why does a meeting in a boardroom in Sydney matter to your house in Paddington or North Lakes? It's all about the domino effect. When the rba cash rate sits at 4.35%, as it has through mid-2026, it sets the floor for what banks charge. A higher rate usually means banks will hike their variable home loan rates within days. But it doesn't stop there. It also changes the fixed rate deals offered to people who want to lock in their repayments. Even if you aren't looking to buy today, these shifts change your "borrowing power." When rates are higher, banks are more cautious about how much they will let you take on, which might change your plans for that next big move.

Tracking the RBA Cash Rate Trends in 2026

As we move through the middle of 2026, the atmosphere around the kitchen table feels a bit different than it did a couple of years ago. The Official RBA Cash Rate Target has remained steady at 4.35% for several months now. After the rapid, heart-thumping rises of the previous years, we have finally entered a "levelling out" phase. It is a welcome relief for many Brisbane families who were tired of checking their bank apps every month just to see another increase.

Don't let the lack of movement fool you into doing nothing. When the RBA hits the pause button, it is actually a green light for you to take a breath and look at your options. Many people think they should only call a broker when rates are falling, but that isn't quite right. Stability in the cash rate is the perfect time to review your home loan structure. It gives you a clear baseline to work from without the goalposts shifting every few weeks. If your rate hasn't moved but your bank's competitors are offering better deals, you are essentially paying a "waiting tax."

Inflation vs. The Cash Rate

The RBA has a very specific job. They want to keep inflation between 2% and 3%. It is like trying to keep a kite flying at just the right height. In May 2026, inflation was sitting at 4.0%, which is still a bit higher than their sweet spot. This is why the rba cash rate has stayed up at 4.35% rather than dropping back down quickly. For us in Brisbane, this means the cost of living stays a bit sticky. Whether it is the price of a flat white in CBD or your weekly grocery shop, the RBA keeps rates higher to try and bring those prices back into line.

What Experts are Saying for the Rest of 2026

Opinions among the big bank economists are a bit split right now. Some are crossing their fingers for a rate cut by the end of the year, while others suggest we might be staying at this level well into 2027. The biggest danger is waiting for a "perfect" rate that might never arrive. Andrew’s perspective is simple: focus on your personal budget, not just the RBA headlines. If you are feeling the pinch today, it is much better to find a more competitive deal now than to gamble on what a board might decide in six months. Your mortgage is your biggest expense, and taking control of it shouldn't depend on a news bulletin.

The Lender Gap: Why Your Rate Isn’t the RBA Rate

Have you ever noticed that when the news says the rba cash rate is 4.35%, your bank statement says something much higher, like 6.25%? It feels a bit like a bait and switch, doesn't it? The truth is that lenders are businesses, not government departments. They don't have to follow the RBA's moves exactly. While the government explains how the RBA uses the cash rate to manage inflation, your bank is busy calculating its own profit margins and operating costs.

One of the biggest frustrations for Brisbane homeowners is the "Loyalty Tax." Banks often save their absolute best deals for brand new customers to get them through the door. It is a bit of a kick in the teeth for long-term locals who have been with the same bank for years. This tax means you could be paying 0.5% more than the person who just signed up yesterday. Over a year, that is thousands of dollars staying in the bank's pocket instead of yours. Andrew’s role is to look past the marketing and find the lenders who haven't passed on the full "buffer" to their customers.

You also need to know the difference between the headline rate and the "Comparison Rate." The comparison rate is the one that actually matters because it includes the fees and charges banks like to hide in the fine print. It is the only way to compare two loans fairly. If a bank has a low headline rate but massive monthly fees, the comparison rate will expose the truth.

Understanding Lender Margins

Banks add a margin on top of the rba cash rate to cover their staff, branches, and profits. The good news? Not every bank has the same margin. Some lenders are "hungrier" for business in the Brisbane market right now and are willing to trim their profits to win you over. Getting a home loan pre-approval Brisbane is a brilliant way to lock in a better margin before you even start looking at open homes. It gives you a clear boundary for your budget and shows lenders you are serious.

Variable vs. Fixed Rates in a 4.35% World

Choosing between variable and fixed rates can feel like a gamble. Variable rates offer great flexibility and features like offset accounts, but they leave you open to RBA risk. If the board decides to hike, your repayments go up. Fixing your rate provides peace of mind while the RBA is in a "holding pattern," but you might feel stuck if rates start to drop later. A popular Brisbane strategy is the "split loan." You fix a portion of your debt to keep your budget safe and leave the rest as variable. It is a simple way to hedge your bets and get a bit of both worlds.

Managing Your Mortgage When Rates Move

It is one thing to understand the news, but it is another thing entirely to know what to do when that news hits your bank account. You don't have to be a passenger in your own financial life. There are a few simple, practical steps you can take right now to make sure the rba cash rate doesn't dictate your entire lifestyle. Even when the board decides to hold rates steady, as they have at 4.35% recently, you can still find ways to save.

First, go and find your "Statement Rate." It is usually buried in the small print of your monthly bank statement or hidden deep in your banking app. Don't just look at the dollar amount you pay each month; look at the percentage. If you haven't checked this in the last year, there is a very high chance you are paying more than you should. Second, if you have any savings at all, make sure they are sitting in an offset account. This is a separate account linked to your loan where every dollar you have "offsets" the debt the bank charges interest on. It is like a protective shield for your money.

Third, if your budget allows for it, consider making small extra repayments while rates are stable. This helps you build "equity" faster, which is basically the portion of the home you actually own. Finally, set a reminder to review your loan every 12 to 18 months. The mortgage market moves fast, and what was a great deal in 2025 might be a bit of a rip-off by late 2026. Reviewing regularly is the only way to make sure you aren't quietly slipping into that Loyalty Tax we talked about earlier.

The Power of Refinancing in Brisbane

Sometimes, the best way to manage a rate move is to move your loan entirely. Moving from a 6.50% rate to a 5.99% rate might not sound like a huge jump, but for a typical Brisbane family, that could mean hundreds of dollars back in your pocket every single month. Refinancing isn't just about chasing the lowest number, though. It is also about getting better features that work for you, like a redraw facility or multiple offset accounts. If you are managing more than one property, you might want to refinance investment property loan Brisbane to ensure your portfolio is working as hard as possible while the rba cash rate stays at these levels.

Planning for First Home Buyers

If you are still trying to get your foot in the door, the cash rate plays a huge role in your planning. A higher rate means the bank is stricter about how much they will let you borrow. It also means you might need a slightly larger deposit to feel comfortable with the monthly repayments. You can use a stamp duty calculator qld to see how much of your savings will go to the government and how much you have left for the actual house. Andrew’s best tip for first-timers is to get a "health check" on your borrowing power before you start falling in love with houses in Paddington or North Lakes. It is much better to know your limits early so you can shop with confidence.

Ready to see if you can do better? You can book a free chat with Andrew to see how your current rate compares to the rest of the market.

How Andrew at Brisbane City Home Loans Navigates the RBA Cycles for You

Does the constant talk about the rba cash rate make you want to put your head in the sand? It is completely understandable. Most people just want to know they are getting a fair deal without having to spend their weekends reading economic spreadsheets. That is where Andrew comes in. Instead of you having to call every bank in Australia yourself, he does the legwork for you by comparing over 60 different lenders at once. He knows which ones are hungry for your business right now and which ones are just resting on their laurels.

The best part? This service doesn't cost you a cent. It might sound too good to be true, but it is just how the industry works. The lenders pay a commission to the broker for finding them a great customer like you. This means you get expert advice and a professional negotiator in your corner without adding another bill to your monthly budget. Andrew takes care of the "heavy lifting," from the mountain of paperwork to the back and forth negotiations with the bank's credit department. You get the result you need while you focus on your family or your job.

You also won't be dealing with a faceless call centre or an automated chat robot. When you have a question about your mortgage, you talk to Andrew directly. There is no waiting on hold for forty minutes just to get a generic answer from someone in a different time zone. It is a one on one conversation with a real person who actually cares about your financial security and understands the Brisbane market inside out.

Our Simple 3-Step Process

- Initial Chat: We start with a relaxed conversation about your goals. Whether you are looking at your first home in Chermside or wanting to refinance a property in Indooroopilly, we talk about what you actually need for your future.

- The Comparison: Andrew takes your situation to the market. He sifts through the options to find the ones that beat the "loyalty tax" and align with the current rba cash rate environment.

- The Result: Once you pick the winner, we handle the application from start to finish. We keep you updated at every step until the settlement is sorted and you can finally breathe easy.

Why a Local Brisbane Broker Wins Every Time

Why choose a local? Because Brisbane isn't just a spot on a map to us. Andrew understands the local suburbs and property values from the CBD out to the growth corridors. He knows that a house in a certain pocket might be valued differently by different lenders, and that knowledge can be the difference between an approval and a "no." It is about finding a loan that fits your life, not just the bank's bottom line. You deserve a guide who is deeply experienced but remains entirely accessible, making the whole daunting process feel straightforward and manageable.

Take Control of Your Brisbane Mortgage Today

The rba cash rate might be decided in a boardroom far away, but the impact is felt right here in your own home. You now know that a steady rate doesn't mean you should stay still. Whether it is avoiding the sneaky loyalty tax or finally setting up that offset account, you have the power to change your financial future. You don't have to tackle the banks on your own or spend hours guessing which deal is actually the best one for your family.

Andrew is ready to do the hard work for you. He compares over 60 lenders to find a rate that gives you a fair go, and as a Brisbane-based expert, he understands our local market better than any national call centre ever could. This service is 100% free for you because the banks pay the commission, not the borrower. It is about getting professional guidance without the stress or the price tag. Book a free, no-obligation chat with Andrew today and see how much you could be saving. You have worked hard for your home; let's make sure your loan is working just as hard for you.

Frequently Asked Questions

Will the RBA cash rate go down in 2026?

The honest answer is that experts are currently divided. While some economists are hopeful for a cut toward the end of the year, others believe the rba cash rate will stay at 4.35% until inflation stays consistently within that 2% to 3% target. Since inflation was still sitting at 4.0% in May 2026, the board is being very cautious. It is usually better to plan your budget around the rates we have today rather than banking on a drop that hasn't happened yet.

How often does the RBA change the interest rate?

The RBA board meets eight times a year to review the economy and decide if the rate needs to move. These meetings follow a set schedule, and the decision is always shared with the public at 2:30 pm on the Tuesday of the meeting. They can choose to increase the rate, decrease it, or keep it exactly where it is. In 2026, we have seen a lot of "holds" as the board waits to see how previous changes are working.

Does a cash rate increase always mean my mortgage will go up?

If you have a variable rate loan, it almost certainly does. Banks usually pass on the full increase to their variable customers within a few days of the announcement. However, if you are on a fixed rate, your repayments stay exactly the same until your fixed term ends. Lenders are independent businesses, so they don't have to follow the RBA exactly, but they almost always do when rates are heading up.

What is the difference between the cash rate and the interest rate I pay?

Think of the rba cash rate as the wholesale price banks pay for money. The interest rate you pay on your mortgage is that wholesale price plus the bank's own "margin." This margin covers the bank's staff, buildings, and profit. This is why there is a gap between the official 4.35% rate and the 6% or 7% you might see on your own home loan statement.

Can I switch from a fixed rate to a variable rate if the RBA cuts rates?

Yes, you can switch, but you might have to pay what is called a "break fee." This is a cost the bank charges for ending your fixed contract early. Sometimes these fees are small, but they can also be quite expensive depending on how much rates have moved. It is a good idea to have Andrew check the numbers for you to see if the savings from a lower rate are bigger than the cost of the fee.

How much can a mortgage broker really save me compared to a bank?

A broker can often save you thousands because they aren't limited to just one bank's products. While your current bank might only have a few options, Andrew compares over 60 different lenders to find the one that is actually being competitive. Since lenders often charge existing customers a "loyalty tax," a broker helps you find the new customer deals that the big banks usually keep for themselves.

Is it better to fix my rate in Brisbane right now?

This really comes down to your own life and how much you value certainty. Fixing your rate means your repayments won't budge, which is brilliant for sleeping better at night if you are on a tight budget. The downside is that you might miss out if rates fall, and you usually lose features like an offset account. Many Brisbane families choose a "split loan" to get the safety of a fixed rate on one part and the flexibility of a variable rate on the other.